The Global Calcuttan Magazine

The Global Calcuttan Magazine

WHY MARKETS LOVE MODI

Everyone with money in play loves Narendra Modi, the man likely to be the next Prime Minister of India.

Everyone with money in play loves Narendra Modi, the man likely to be the next Prime Minister of India.

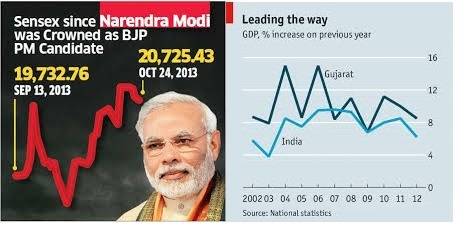

India’s Nifty and Sensex indices rose to their second consecutive record-breaking highs on Monday as blue-chips jumped on rising hopes that exit polls are right. Investors and the Indian press have now official pre-ordained Narendra Modi as Prime Minister, with his political party and its allies in firm control of parliament. If such a case comes to fruition, that would give Modi a mandate for some pro-business policies in his first 100 days in office.

The Sensex rose over 2.5% to a record high at 23,572.88, while the Nifty rose

2.35% to a record breaking 7,020.05. The Wisdom Tree India Fund IFN -0.9% (EPI) settled 3.77% higher today, clobbering the benchmark MSCI Emerging Markets Index by more than 200 basis points. Year to date, the hotly traded India exchange traded fund is up 17.6% while emerging markets are up 1.26%.

“There’s been a deep bottle necking of infrastructure projects in India, but Modi has a great track record of de-bottle necking infrastructure projects in his state of Gujarat,” says Joel Wells, portfolio manager at Alpine Woods Capital Investors in New York.

Modi is the chief minister of Gujarat, which is the Indian equivalent of governor. He’s held the position since 2001 and has been heralded by many for doing away with the traditional bureaucratic barriers to development. Road projects get licensed to build within a two year period, nearly half the norm for India. Steel mills are giving the Ok to build in shorter periods of time.

Some foreign money managers believe Modi can turn India into on big Gujarat, if not a little less efficient. Foreigners have helped push Indian equities higher because of Modi. “The percentage of infrastructure projects in Gujarat trends much more than India overall,” says Wells. “The country thinks he can reinvigorate the animal spirits in India to develop.”

The curtains came down on Monday for India’s massive five-week long election with a record high turnout of 66.38%. That beats the 64.01% turnout in 1984 as Indians angrily took to the polls after the assassination of Prime Minister Indira Gandhi. A little over 58% turned out for the last general election in 2009.

Results are due on Friday.

WHY A SAFRON INDIA IS SET TO OUTPACE CHINA

On the face of it, the title of this article will seem absurd to many. While China’s economic growth has slowed, it’s still running at a brisk 7.4% annual rate. Moreover, the Chinese government seems to be successfully slowing credit in order to rein in a burgeoning debt issue. And it’s implementing a plethora of reforms which should propel the next phase of growth.

Meanwhile, India’s a mess. This fiscal year’s GDP will be below 5% and near decade lows, government and corporate debt is high, the current account deficit has been out of control until recently, inflation reached double-digits late last year, business confidence and investment are at extreme lows and corruption remains rampant.

Dig a little deeper though and the picture doesn’t appear as favourable for China’s economic prospects vis-a-vis India’s. First, it’s highly probable that China’s GDP growth rate is slowing much more than the fraudulent figures put out by the government (I’m not picking on China here as many governments are guilty of this). Second, credit tightening in China will almost certainly take years rather than months given the boom which preceded it. Third, Chinese economic reform will be a drag on growth in the near-term, as can already be evidenced by the crackdown on corruption and its impact on retail consumption.

On the flip side, there are many signs that India’s economy may have bottomed. The current account deficit has significantly eased, the currency has stabilised, inflation has substantially pulled back and corporate earnings are improving. With inflation down, interest rates will soon be cut, which may prove the catalyst for the next investment cycle. The election of a new, economically-friendly government should ensure an acceleration in investment and improved productivity.

There are other positive developments which augur well for India too. For instance, there’s an ongoing boom in the agricultural sector with rising investment and wages. This has resulted in India becoming a net food exporter – an important development given the country’s dependence on agriculture.

For a long time, India’s decentralised, often chaotic economic model has been seen as inferior to China’s authoritarian, top-down model. A reappraisal of that view may soon be in order.

How India became a mess

Morgan Stanley’s Ruchir Sharma has noted that India seems to go through cycles of economic crisis and reform every decade or so. In 1991, a balance of payments crisis preceded widespread economic deregulation which is credited for driving the rapid economic growth of the following two decades. In the early 2000s, another crisis resulted in further deregulation and privatisation of key industries.

Here we are about ten years later and there are economic troubles again. GDP growth has slipped below 5%. Inflation peaked in double digits before marginally declining of late. The fiscal and current account deficits have widened sharply.

The government is again largely to blame for the problems. The ruling Congress Party fell into the trap of thinking that economic growth in the high single digits during 2003-2007 was perfectly natural. But it was just the result of reforms from prior governments.

In response to the 2008 crisis, the ruling party initiated a large stimulus package. This worked for a time as the economy recovered faster than most other emerging markets. But combined with large-scale subsidies to bribe rural voters, to the tune of 2.3% of GDP, inflation soon lurched out of control. A lack of reform driven by infighting in the Congress Party and a judicial crackdown on political corruption didn’t help.

Foreign investors and bond rating agencies became increasingly nervous about India. In 2012, the ratings agencies threatened to downgrade the country’s sovereign rating to junk status. Mid last-year, the rupee tanked as foreign investors grew concerned about the current account deficit following hints of QE tapering at that time.

These events were enough to spark the government into action. It’s since liberalised foreign investment in retail and airlines. It’s also started to cut back on energy and agricultural subsidies. More recently, the new central bank governor hiked interest rates to stabilise the currency and tame inflation.

Signs the economy has bottomed

There are a number of signs though that India’s economy may have bottomed and better times lay ahead:

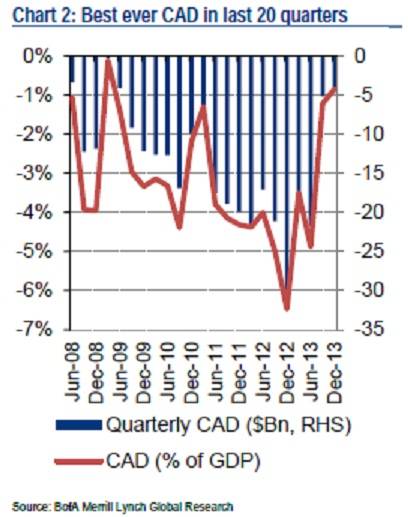

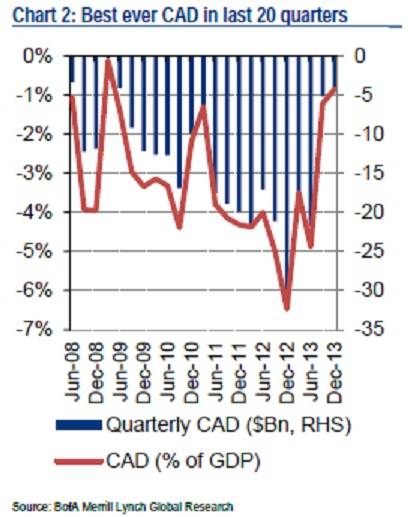

1) The current account deficit (CAD) has eased significantly. The last quarter saw the lowest CAD number in five years due to improved exports and lower gold imports. Bank of America Merrill Lynch forecast India’s CAD will be 2% this fiscal year compared with 5% in 2013.

India CAD

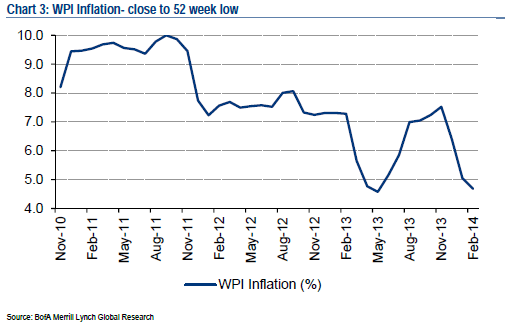

2) Inflation has pulled back. Due to lower food prices, WPI inflation is at its lowest level in more than four years.

India inflation

3) The rupee has stabilised. Interest rate hikes and the declining CAD have helped.

4) Corporate earnings seem to be improving. The earnings revision ratio has been rising for the past eight months. Yes, it’s still not great but at least it’s heading in the right direction.

India earnings revision cycle

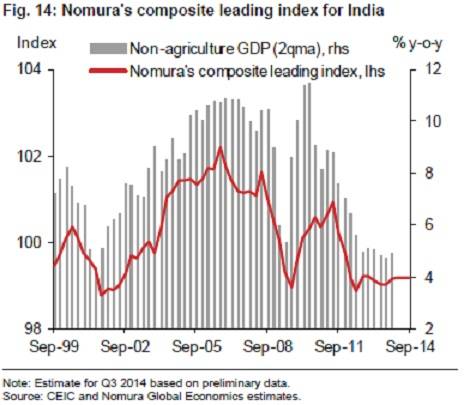

5) Nomura’s composite leading index for India suggests growth is bottoming out.

India – nomura leading indicator

The key to an economic recovery though is business investment. There are tentative signs that this may be set to turn around:

Business confidence, while low, has improved of late in anticipation of a new government coming into power.

Regulatory constraints for new projects should be eased post election. A Cabinet Committee on Investments has already started to reduce bottlenecks, but this should soon accelerate.

Higher interest rates are forcing Indian companies to reduce leverage by shedding assets. The process of decreasing debt, particularly among infrastructure companies, is necessary for businesses to be in a position to accelerate investment.

Asia Confidential doesn’t foresee a quick turnaround in capital expenditure given high corporate debt levels. But with the prospect of sharply declining interest rates and a new economically-friendly government soon in power, the conditions are in place for a gradual pick-up in business investment.

Modi: friend or foe?

The big question is whether the almost-certain-to-be new leader, Narendra Modi, can deliver on the inflated expectations of him. India’s stock market is certainly answering in the affirmative as it hits new highs (though it’s noteworthy that small caps have significantly lagged).

Modi’s economic track record is undoubtedly impressive. He’s been chief minister of Gujarat, a state with 60 million people, for 12 years. During that time, he’s cut red tape, built substantial infrastructure and contained corruption. Business and investment have thrived. Gujarat GDP has grown 3x under Modi’s leadership. The state now produces 25% of Indian exports yet accounts for just 5% of the nation’s population. Most social indicators in the state have also improved under his watch.

As leader, Modi has promised to replicate his Gujarat policies of improving infrastructure, reducing regulatory hurdles for businesses and ultimately achieve higher growth rates. Granted, he’s been vague on how he’s going to finance some of his promises. Given the fiscal situation, there’s not much room for a substantial boost in spending.

The big blight on Modi’s track record is his hardline Hindu nationalism. In 2002, Muslims in the Gujarati town of Godhra set fire to a train carrying Hindu pilgrims back from a town in Uttar Pradesh. 59 people died on the train. After the attack, Hindu groups called for a protest. This resulted in several days of violence directed at Muslims. 1,000 died and 200,000 were displaced.

Being chief minister at the time, Modi had the option to ban the protest or call in police, but he chose not too. This was condemned at subsequent investigations. And Modi’s refusal to apologise for the incident continues to anger Muslims. The US actually revoked Modi’s visa, suggesting “he was responsible for the performance of state institutions” in the riot.

The facts of this incident are damning but must be weighed against his economic track record and leadership qualities. They must also be weighed against the ineptitude and arrogance of the governing Congress Party over the past decade and for much of the past 50 years.

What matters most though is the opinion of the Indian voter. There’s a chance that Modi could win an outright majority of votes in the general election, which would allow him to rule without coalition partners. The most probable outcome is that he’ll win a near-majority and will be able to build a coalition with a small number of partners.

By voting for Modi, Indians will be clearly saying that they’re tired of the Congress Party’s policies of protectionism, the bribes disguised as subsidies and corruption which goes along with these. They’re demanding policies to promote economic growth, development and jobs. And they want decisive leadership rather than bumbling and infighting.

It may be a stretch to suggest that voters favour market-driven solutions over government-driven ones. But the tide has certainly swing in that direction.

Ultimately, Modi is expected to be given a strong mandate for change and his business-friendly credentials bode well for the country’s economic prospects.

Broader, ignored positives

Besides a bottoming economy and new, potentially improved leadership, there are also several other positive developments which point to a brighter future. India’s much-maligned legal system and decentralised political system have proven strengths of late.

It’s the judiciary which has led the way in fighting corruption. There’s little doubt that corruption remains a huge issue in India. There are some estimates that it’s cost the country US$80 billion over the past decade. According to Transparency International, India ranks 94 of 177 countries in its global corruption perception index, behind the likes of China and Brazil, both hardly paragons of clean administrations.

The courts have been central to curbing some of the rampant corruption. The cancellation of 122 mobile phone licences and jailing of the telecommunications minister in 2012-2013 being but one example.

It’ll be up to Modi to accelerate the crackdown on corruption. It’s crucial that he does as corruption takes valuable money away from productive investments which can boost economic growth and keep inflation in check.

Undoubtedly, political decentralisation has helped the spread of corruption. But the upside from decentralisation is that India’s growth has been shared by rural areas as much as the cities (unlike in China).

In fact, rural areas in India are booming. Wages have risen by close to 15% per annum over the past ten years, compared to city wages which are down more than 2% over the same period.

Decentralisation provides part of the answer for the boom. Urbanisation – people moving from country to city – has also played a role as it’s resulted in a tightening in the rural labor force and contributed to the rise in wages and investment.

A moment in the sun

All of the above isn’t to suggest that India will displace China as Asia’s next economic giant. Far from it. With GDP per capita of just US$1,250, India still has an enormous way to go to catch up with China (GDP capita of US$6,700) and the rest of the developing world (GDP per capita of close to US$10,000).

What Asia Confidential has sought to demonstrate instead is that India has more scope to surprise than China on the economic front. Part of that is because India’s coming from such a low base.

Moreover, this author can foresee a time in the not-too-distant future when India’s economic growth matches, and likely surpasses that of China. The media may then be lauding the superiority of the Indian growth model over China’s!

AC Speed Read

– Despite slowing, China’s economy is still growing at a much faster clip than India’s.

– But that may be about to change with signs that India’s economy has bottomed while China faces serious downside risks.

– With inflation falling in India, interest rates there are set to drop and this, combined with a new, business-friendly government, should provide the impetus for the next business investment cycle.

– For a long time, India’s decentralised economic model has been viewed as inferior to China’s authoritarian, top-down model. A reappraisal of that view may soon be in order.