The Global Calcuttan Magazine

The Global Calcuttan Magazine All the President’s (offshore) Men

“Finally, our plan will bring back trillions of dollars from offshore … that will come pouring back into our country that will be put to work and will be spent by our companies that could never get the money back for many years…We’re rebuilding America.” – Donald J. Trump on his tax reform initiative.

CONTRIBUTING EDITORS & STAFF

While the American public reacts to charges of money laundering and other improprieties, made last week against Donald Trump’s former campaign manager, an enormous leak of financial information on the Word’s elite, exposes the secret offshore machinations of Trump’s inner circle.

Dubbed, ‘The Paradise Papers’, the leak, which is comprised of 13.4 million documents – and rivals the now infamous Panama Papers in magnitude and range – comes from a Bermuda-based law firm called Appleby, its spin-off corporate services arm Estera, as well as the Singapore-based Asiaciti Trust.

Among those on the blue-chip client list are world leaders, the estate of Queen of England, and such companies as Apple and Nike. Conspicuous for Trump is the number people connected to his administration who are clients, and have been involved in questionable transactions.

Notably, his commerce secretary, Wilbur Ross and son-in-law cum senior advisor, Jared Kushner whose array of responsibilities range from government reform and management of the domestic opioid crisis to brokering peace in the middle east, were involved in transactions that lend credence to the allegation that Russia colluded with Team Trump to turn the 2016 US election.

Perhaps less perilous for the US President but equally troubling is how the revelations undermine his policy objectives. A key campaign promise that countered claims that billionaire Trump’s policies would favour his peers, was to legislate the repatriation of offshore cash bringing it legally into the American economy. Just a few days ago, Trump had reiterated this view in discussing his tax plan: “Finally, our plan will bring back trillions of dollars from offshore … that will come pouring back into our country that will be put to work and will be spent by our companies that could never get the money back for many years. Bring the money back. We’re rebuilding America.”

Such rebuilding may well be order if Trump’s braintrust keeps chipping away at the country’s GDP with pickaxes made of gold. With combined net worth exceeding $10 billion, here are the golden ax-wielders:

TOP-ADVISOR AND SON-IN-LAW, JARED KUSHNER

Amidst the documents comes the damning revelation that a Kremlin-connected tech magnate, Yuri Milner (whom Forbes Magazine called Russia’s most influential tech mogul) invested $850,000 In Cadre, a small real estate firm co-founded by Kushner. Milner’s investments had previously been focused on internet technology. While Cadre does leverage the internet as a platform to make deals, its revenue comes from real estate ventures, seemingly a departure from Milner’s investment model. What’s more is that Kushner’s stake in Cadre was not disclosed when he joined the administration of his father-in-law.

Transactions involving Milner threatening blowback against he Trump administration don’t end with Kushner. What seem like inculpable investments social network giants Facebook and Twitter fall under scrutiny due to the source of funds: VTB Bank, the Kremlin’s most favoured financial institution; and a shell company funded by a subsidiary of Gazprom, the Russian state controlled energy giant. This raises questions given that US intelligence agencies have reported that the two largest social network and microblogging platform, respectively, had been used in 2016 by actors based in Russia to propagate misinformation heavily favouring Trump’s presidential campaign and disparaged Hillary Clinton’s.

For his part, the Kushner associate claims that he was an early investor in these platforms, particularly Facebook, and they took place long before Trump had declared his run for the presidency. In fact, the revelations alone are hardly a smoking gun. Still, taken with the alarming discovery that the money was sourced from the Russian government, ended up in Facebook and Twitter’s accounts – and that these platforms were used extensively to favour Trump, the information may well prompt Special Counsel, Robert Mueller to check Kushner and Millner for the proverbial gunshot residue.

Adding to the intrigue is the fact that Milner’s financier, Gazprom Bank (a subsidiary of Gazprom) is run by members of Putin’s inner circle. That Putin’s son-in-law (more about him, below) was appointed ‘Chief Legal Counsel for Foreign Economic Activity’ before he had finished his legal studies, and then graduated to Chief Legal Counsel upon graduation from law school at St. Petersburg State University, is a matter of public record.

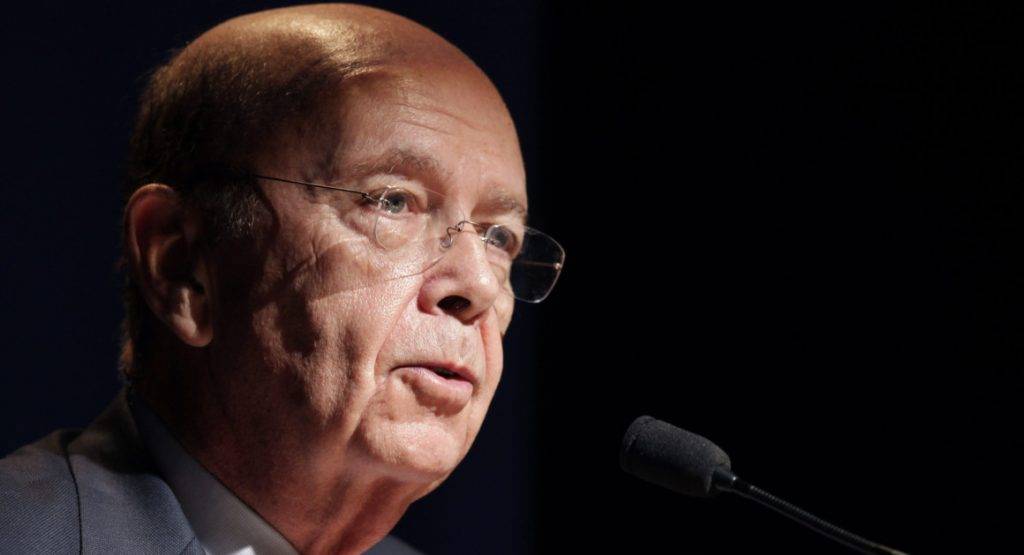

COMMERCE SECRETARY, WILBUR GOSS

At least as problematic for the Trump administration is the discovery, in the leaked papers, that Trump’s Commerce Secretary, Wilbur Goss is substantially and very lucratively in business with Vladamir Putin’s son-in-law.

The leaked documents as well as public record reveal that billionaire, Goss, who is also a close friend of Trump’s has a large stake in the shipping company, Navigator, through a series of offshore investments. Navigator, in turn, operates a partnership with the large petrochemical processing firm Silbur, worth almost $ 3 billion, and co-owned by Krill Shamalov. Shamalov, also reported to be a billionaire, happens to be married to Putin’s daughter.

This means that the man charged with heading the government department responsible for promoting economic growth and, among other functions, the administration of international trade, stands to benefit financially from business activities of at least one member of Putin’s family. Shamalov is the son of one of Putin’s oldest friends, and has been identified as a repository of Putin’s hidden wealth along with Putin’s daughter. That would, in substance, put Goss in business with Putin, himself. In the murky nexus of international commerce and politics, such a connection doesn’t get more direct than this!

As Russian aggression in the Crimea heightened, so too did Navigator’s relationship with Silbur, earning the American partner a whopping $68 million in 2014. In fact, Shamalov’s $1.3 billion stake in Silbur had been financed by Gazprom Bank, which was then sanctioned by the Obama Administration. Kiril’s brother Yuri was director and Deputy Chairman of the bank at the time. He was also chairman of Gazfond, an investment fund controlling the assets of Gazprom pensioners. The fund also controlled Gazprom Bank. The US had sanctioned the bank because it was deemed to be the preferred bank of the Russian elite with ties to Putin. The Shamalov brothers are only two of a host of Putin cohorts associates holding key positions with the bank or its associated entities.

Ross’ profits in Navigator doubled when US Sanctions prevented Silbur from accessing foreign capital markets. The apparent distress for Silbur was a smokescreen: the Russian government invested $700 million the Ust-Luga port, west of St. Petersburg where Silbur was given exclusive rights to ship liquefied gas through Navigator to Scandinavia; and near the end of 2015, Silbur received a $1.3 billion loan from the Russian government payable at one-third the market rate.

When navigator went public, buoyed by its deal with Silbur, Ross made a killing in excess of 200% profit, prompting him to boast about hitting a “home run” with the company. Though his press secretary, James Rockas has tried to distance Ross from the company, saying he never held a majority stake, such claims are contradicted by public records. Rockas also falsely claimed the Silbur deal was struck prior to Ross making his investment in Navigator. In fact, Ross elevated the level of his investments in Navigator after the deal.

When wealthy people take public office, many vest their holdings into a blind trust, so their activities as government officials are unaffected by their business dealings. Trump never did this, and Goss followed this shady example. That said, he ought to have disclosed the dealings to US ethics authorities. Perhaps fearing the obvious red flags that would have been raised, Goss disclosed only that he was keeping investments in a pair of obscurely named holding companies, but did not specify whether he would also retain their interests in Navigator and its lucrative contract in Russia.

Daniel Fried, an assistant secretary of state for European and Eurasian affairs under George W. Bush, told The Guardian that Ross’s connection to “cronies of Putin” threatened to undermine US sanctions.

“I don’t understand why anybody would decide to maintain this kind of relationship going into a senior government position,” he said. “What is he thinking?”

Indeed, Peter Harrell, a senior state department official under Barack Obama, who worked on sanctions against Russia, said: “I’m frankly surprised. Maybe I shouldn’t be, given that with this administration, there seems to be a Russian in every closet.”

Karen Dawisha, the director of Russian and post-Soviet studies at Miami University, Ohio, said it should be assumed that Putin benefited from the prosperity of companies run by his relatives and close associates.

“Shamalov is a very important member of Putin’s circle and there is no question that he is closely trusted,” said Dawisha. “He was not well trained for the job at Sibur, but he was well connected.” Shamalov has a law degree from St Petersburg State University, according to Sibur.

Shamalov stepped down as deputy chairman in 2015, remaining a director. This year, he reduced his 21.4% stake in the company, which was worth about $2.85bn, to 3.9% just as journalists were looking into Sibur’s connections to Ross. The reason for this billion-dollar sale was never disclosed.

Shamalov sold his stake to Sibur’s largest shareholder, Leonid Mikhelson, CEO of gas producer Novakek and according to Forbes magazine Russia’s richest man. The Obama administration twice imposed sanctions on Novatek, once in 2014 over Ukraine and again in 2016 in reaction to Russian interference in the US election.

Goss and Kushner’s dealings are so tainted, they are swimming in vodka.

But it doesn’t end, there.

(Photo by Alex Wong/Getty Images)

US SECRETARY OF STATE, REX TILLERSON

Secretary of state Rex Tillerson may have been in a war of words with Trump, recently but he is also a member of the richest one percent of America’s population with net worth at around a third of a billion dollars. Tillerson’s career at Exxon Mobil, chronicling a rise to CEO is a well known success story. However, the leaked papers also name him mas a director of an offshore firm used in a multibillion-dollar oil and gas ventures in the Middle East that became embroiled in controversy.

Tillerson was a director of Marib Upstream Services Company, incorporated in Bermuda in 1997. The company was affiliated with ExxonMobil, the American oil and gas corporation that Tillerson later led as chief executive. At the time, Tillerson was president of ExxonMobil’s Yemen division.

ExxonMobil and Hunt Oil, another Texas-based firm led by Tillerson’s close friend Ray Hunt, ran a $5bn venture to export 61m barrels of natural gas a year from fields in Marib, western Yemen. Hunt had discovered the fields in the mid-1980s and brought in ExxonMobil to help develop them.

Like Iran and Iraq, Yemen’s energy policy evolved into a nationalist one, and the gas-drilling operation came under the ownership of the state. This cut out the ExxonMobil-Hunt venture when its 20-year exploration contract expired in 2005. With barbarians at the gate, the oil companies desperately claimed the Yemeni government had agreed to an extension and sued the poor and least developed middle eastern country for gargantuan $1.6 billion. The case went into arbitration at the International Chamber of Commerce, where the Yemen, the proverbial David, defeated ExxonMobil-Hunt’s Goliath.

The wound suffered by the Americans never quite healed.

So what is Tillerson’s position on the Saudi-led war with Yemen, described by many analysts as a cynical maneuver to gain control of Yemen’s oil and gas? It follows the money – and the interests of his old company: he supports the Saudis even though the United Nations has accused the Kingdom of wanton disregard of human life amounting to possible war crimes – and creating a catastrophic resulting famine not seen since World War II. Hardly surprising, considering Tillerson’s past and the grim fact that there is life after public office, especially for those who’ve helped-out big business. One only needs to ask Dick Cheney of the benefits of pursuing policies that help his friends.

Around 10,000 people have been killed in the Saudi-led war on Yemen of which most are civilians. Aid agencies have warned that the country is at the “point of no return” as roughly 7 million people teeter on the brink of starvation. The World Health Organization (WHO) has reported over 900,000 cases of cholera even as a recent Saudi blockade of the country is preventing humanitarian aid to reach the afflicted. While Trump hasn’t called this fake news (yet), he and his secretary of state, despite their differences are lock in step with one another on backing Saudi Arabia as the situation becomes increasingly catastrophic.

Well, one person’s catastrophe is another’s opportunity.

CHIEF ECONOMIC ADVISOR, GARY COHN

Described by the Wall Street Journal as an ‘economic policy powerhouse,’ Gary Cohn is Director of the National Economic Council – a position that requires congressional assent, and driver of Trump’s tax policy.

The Paradise Papers reveal that for a period of four years, while head of commodities and equities for Goldman Sachs where he went on to be President and Chief Operating Officer, Cohn was listed as either president or vice-president of 22 separate corporate entities based in Bermuda with registered offices at 85 Broad Street, New York City where Goldman Sachs is headquartered. The companies operated in the real estate sector.

Cohn has said he isn’t embarrassed by the disclosure, commenting, glibly: ‘This is the way that the world works.’

Indeed, according The Guardian, Goldman Sachs said it did manage a fund that invested in Asia, but paid taxes on its income from the fund “in all relevant tax jurisdictions”. Of Cohn, the company said it was common for its employees to be officers of its legal entities and they were not paid for these additional roles. Cohn has mentioned nothing about these companies investing in Asia; instead, he maintained that, ‘many of these vehicles were set up to send capital into the U.S. to buy securities, or buy assets in the U.S.’

‘It’s a way to facilitate the international commerce and a way to facilitate moving capital into the U.S.,’ Cohn told CNBC. But why he would hold key positions in companies involved in real estate while head of commodities and equities remains unanswered. Moreover, he mentioned such entities were used to pool international investment, so the profits, in some instances, could be sent to the US. He mentioned nothing about Asia, so why Goldman Sachs would connect Cohn with the continent is confusing. Nobody seems to be pressing either Cohn or Goldman Sachs for answers. Perhaps Bob Mueller will pick up where the media has so clearly left or fallen off.

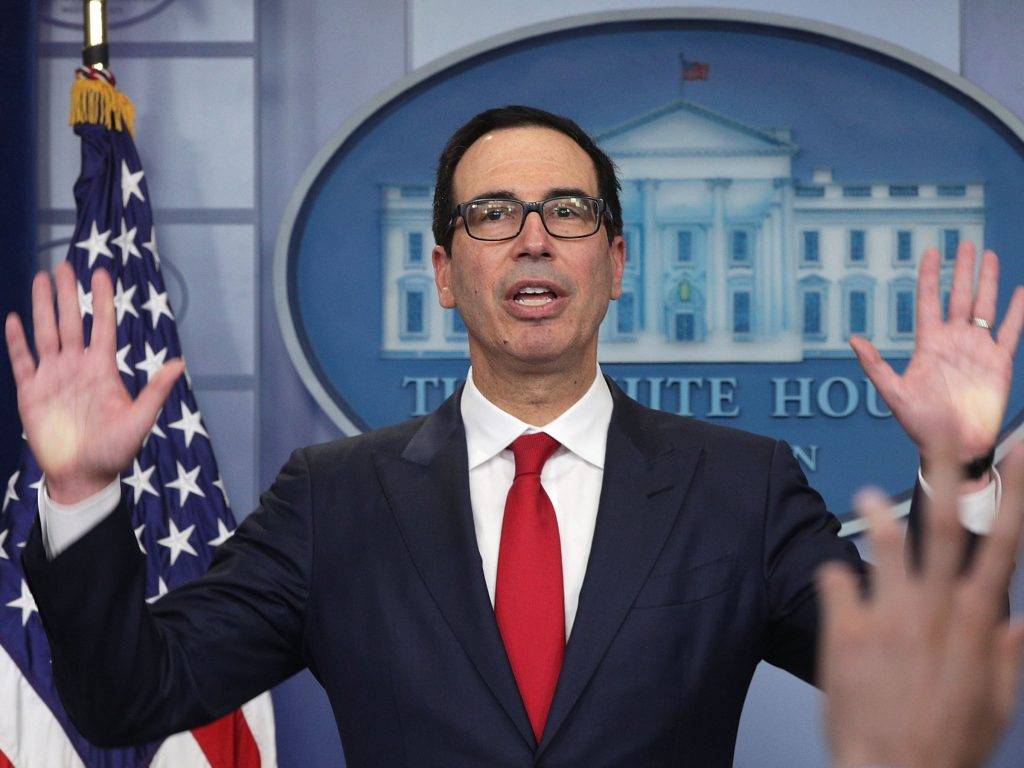

TREASURY SECRETARY, STEVE MNUCHIN

Following predecessors, Trump appointed another Goldman Sachs alumnus as treasury secretary in Mnuchin.

In the 2000s, in part while Mnuchin was Executive Vice President, member of the Management Committee, and Chief Information Officer, Goldman Sachs paid around $74 million in fines and penalties including to the US Securities and Exchange Commission (SEC). Indeed, the year after Mnuchin’s departure after 17 years of service, his former employer paid out $110 million as its share of a global settlement by ten firms with federal, state and industry regulators concerning alleged conflicts of interest between their research and investment banking activities.

Mnuchin’s connection to the Paradise Papers is through CIT Bank. He profited immensely from his sale of OneWest Financial to CIT Bank. As part of the deal, he became a board member, including being Vice-Chairman of the Board of Directors.

During this period, Mnuchin’s former bank financed offshore private jets for wealthy clients, including a billionaire Yemeni businessman whose son is wanted for rape and murder in the UK. The transaction was routine as CIT Bank provided various customers with financing structures for personal aircraft priced at tens of millions of dollars, which customers used to legally avoid sales taxes and other charges.

According to The Guardian, one leaked file from October 2015 shows CIT billing an Isle of Man company $430,993 for an instalment on a $30m Dassault Falcon 2000EX jet. Other files say that the ultimate owner of the Isle of Man company is Shaher Abdulhak Besher.

VICE-CHAIRMAN, FEDERAL RESERVE, RANDAL QUARLES

As Vice-Chairman, Supervision at the US Federal Reserve, Quarles is the Trump Administration’s senior banking watchdog. Someone in his positions should have no conflicts of interest not only in fact but also in appearance.

Quarles is named in the files as an officer of two firms incorporated in the Cayman Islands by the Carlyle Group, the private equity giant where he was a partner until 2013. Detailing transactions between one of Quarles’s offshore vehicles and Butterfield, a Bermuda-based bank in which Carlyle had led a $550m investment in 2010, the files reveal that the stake was one of several distressed banks bought up by a new specialist team at Carlyle, including Quarles, following the 2008 financial crisis.

In November 2013, federal authorities secured court orders requiring a group of US banks to disclose information on Americans “who may be evading or have evaded federal taxes” via undisclosed affiliated accounts at offshore banks including Butterfield. They said 81 such accounts at Butterfield had already been disclosed.

Butterfield said in its last annual report that it was cooperating with US authorities and had set aside $5.5m to pay penalties that may arise from the inquiries.

Quarles told ethics regulators this year that he held assets worth between $5m and $25m in a Carlyle fund that held a stake in Butterfield. He said he intended to sell his holdings in that and most other Carlyle funds.

A Federal Reserve spokesman said Quarles “had no specific responsibilities, was not delegated any responsibilities by the board, and received no income for this position” at the offshore company, and had divested from Butterfield when he joined the government. If this is to be believed, one wonders why the board bothered to keep Quarles on, for surely, if the spokesman is correct, Quarles was dead weight – that is, unless he was not. The Carlyle Group has a history of leveraging useful connections of investors from former Presidents and Prime Ministers, including George H. W. Bush. They would not have engaged Mnuchin as a partner if he was dead weight – this much is certain.

SEC CHARIMAN, JAY CLAYTON

If anyone’s name in the Paradise Papers would raise red flags (red flags on burning flagpoles?) it’s SEC Chairman Jay Clayton. Belying his former role as corporate lawyer defending the interests of Wall Street, as SEC chairman, he is charged with protecting to ensure the free and fair functioning of the marketplace. Within this responsibility comes an important function to keep an eye on the offshore interests of companies and hedge funds.

But Clayton, himself, is a beneficiary of offshore financial protection receiving income from Mount Kellett through a trust set up for partners of Sullivan & Cromwell, the law firm where he worked for many years. In March, he agreed to divest from the fund within 90 days of taking up his SEC post.

Clayton declined to say how much he received annually from the Cayman Islands subsidiary, or to comment on how his involvement offshore would affect his new role as overseer of offshore investments.

Far more odious than anything listed in The Paradise Papers In contained in Clayton’s 278 financial disclosure form. A staggeringly long 28 pages, his disclosure on the Clayton family’s sources of income, which makes most people’s tax returns look like kindergarten homework, is money from a company called WMB Holdings.

WMB Holdings, Clayton explains in a verbose and unhelpful endnote, is a Delaware-based entity that provides “business, financial, and representational services.”

But Rolling Stone reports that this is actually firm whose purpose it is to structure other companies. “You call them up, and 20 minutes later you’ve got a Delaware corporation,” says Jack Blum, an expert on white-collar crime and money laundering who is best known for his investigation of the BCCI scandal.

Such firms, like Appleby’s spin-off, Etera, are used to create chains of legal entities, sometimes ending in offshore accounts, rendering a vanishing trail of financial transactions. They are companies that help make ownership unfathomable, companies blend into the shadows. “If you want to launder money, evade tax or hide assets from a spouse, you can do it,” says Blum.

Clayton’s family seems to have a serious interest in this firm. He lists a series of family trusts containing WMB holdings, most producing high annual dividends, which added up come to over $4 million, annually. Not bad for “business, financial and representational services.”

The endnote claims Clayton has no beneficial interest or control in these holdings, but that his wife and/or children have a “beneficial interest.”

Given just such a company would appear to be subject to SEC oversight, it’s worth asking the nature of his family’s involvement with WMB. His casual attitude towards the disclosure reveals a disturbingly laissez faire attitude when it comes to such companies. Not exactly the crack investigative zeal one would expect of an SEC Chairman.

Clayton has pledged to divest from WMB when his wife has “directly held financial interests” in the company, but not where his wife or his children are “solely a beneficiary.”

The organization, Public Citizen believes that WMB “may also be the parent of Corporation Service Co. (CSC),” another large business services firm with offices in “Delaware, Australia, France, Hong Kong, Singapore, Sweden, and the United Kingdom.”

Among other things, WMB was for some time listed as the parent of a company called CSC Trust Co., now called Delaware Trust Co.

CSC Global claims 2,500 employees as well as 180,000 corporate customers, while also representing 10,000 law firms. The company appears to do more or less the same things that Clayton says WMB does, dealing with creating legal business entities, management of licenses, upkeep of filings, dealing with service of process, etc.

Interestingly, and to Blum’s point, Clayton’s disclosure does not list any interest in CSC. So, although he gives some information about what appears to be a holding company with little to no public profile, the company that boasts of its connections to 180,000 corporations is not mentioned in the disclosure form.

According to Rolling Stone, neither CSC nor Clayton have responded to requests for comment.

Tom Barrack, Colony Capital founder, investor and Presidential Inaugural Committee Chairman – photo by Vladimir Astapkovich/Sputnik via AP

TOP FUNDRAISER AND ‘CONSIGLIERI’, THOMAS J. BARRACK

The billionaire Barrack, who runs a $58 billion real estate trust, has been an integral part of Trump’s brain trust for over thirty years, and is a close friend. They have operated in the same industry around the same properties, even, and The New York Times has called Barrack “one of the few people whom Mr. Trump trusts.” According to Barrack, they speak on a near daily basis.

He was chairman of Trump’s inaugural committee and raised over a hundred million dollars for Trump’s presidential bid, making him a top fundraiser. He also introduced Trump to former campaign manager, Paul Manafort, now indicted on twelve counts including money laundering under Special Counsel Mueller’s investigation of the Trump campaign’s collusion with Russia to turn the election.

Barrack loaned Manafort $1.7 million to refinance a home in the Hamptons. According to a spokesman for Barrack, the loan was in fact to Manafort’s wife. Nevertheless, Barrack said the loan was repaid in 14 months, and this was the only financial transaction between them.

Manafort’s charges are mainly linked to overseas income allegedly protected by a network of offshore accounts in Cyprus.. The Intercept reports that, “in what is likely an extraordinary, only-in-the-Trump-administration coincidence, prosecutors allege that most of the offshore accounts were tied to the Bank of Cyprus. Commerce Secretary Wilbur Ross was vice chair of that bank until he divested to join the administration.”

Barrack was likely unaware Manafort’s other dealings, and was simply helping out a friend, generosity for which he has become known in his circle. On Manafort’s side, however, the loan fits the pattern of serial indebtedness sought by Manafort to keep his criminal enterprise going – and described in the Special Counsel’s indictment of him. The scheme involved a cycle in which Manafort used newer mortgages to pay off older ones – the steady flow of credit gave him cash infusions while allowing him to evade taxes. Manafort is also accused of telling an assortment of lies to get bank loans at more favorable interest rates so that when the loans had to be repaid, he wasn’t losing much of his offshore fortune. The indictment even references a Hamptons home as one of the vehicles for alleged money laundering at around the same time. The rate of interest on the loan, if any, has not bee publicly reported.

Barrack’s association with Trump goes back to the late 1980s when, as a trusted representative of the Bass family who owned the marquee property, The Plaza Hotel, which Trump could see from his office window, brokered Trump’s purchase of prime property. “You have the Plaza,” Barrack would recall Trump saying over the phone. “I want it.” Barrack made it happen, and his reputation with Trump as a deal-maker was forged.

He was one of the financiers who helped bail out Trump when he nearly went under during the early nineties.

Barrack’s name is mentioned in the Paradise Papers in connection with offshore subsidiaries of Colony NorthStar, of which he is CEO. In 2011, Appleby helped devise a rolling credit facility (reference back to the Manafort arrangement) linking Barrack’s US-based investment funds with a pair of Cayman-Islands-based subsidiaries dealing in troubled real estate, which the lawyers asked him personally to approve.

A confidential chart in the leaked documents suggested money would flow from the funds in Delaware to a Cayman Islands entity, Colony Distressed Credit Fund II Feeder A, which was “exempted”, meaning it paid no local taxes. The chart suggested the money would then be repatriated in a complex web to a separate Delaware subsidiary closer to the parent company.

Barrack has not admitted to being aware that Colony was passing money through a subsidiary in the Cayman Islands or whether the feeder funds were set up to reduce tax payments, though he hasn’t pleaded ignorance either. The firm has said: “Colony NorthStar is in strict compliance with the letter and spirit of all applicable rules for cross-border business, as we have been for more than 25 years.”

OTHER MEMBERS OF TRUMP’S MURKY MONEY CIRCLE

- Ben Carson, Housing and Urban Development

- Secretary.Jon Huntsman, Ambassador to Russia,

- Kenneth Jester, Ambassador to India, and

- Carl Icahn, Senior Advisor

WHY IS THIS SIGNIFICANT

The files detail the transactional environment in which tax abuses are rampant as well as the ways in which the wealthiest one percent, be they people or companies, shelter their wealth from regulatory scrutiny. The activity in many instances are shown to have been hidden in a complex web of transactions, which teeter on the razor’s edge of laws. In other cases, the transactions may be illegal and are being investigated by authorities.

The leak tells a story of shell companies, hidden companies and many other proxies registered tax havens to reroute wealth or hold assets in property, aircraft, yachts, investments in stocks and shares, or make wealth disappear altogether to secret bank accounts. The hidden wealth is vaster than previously imagined. The papers reveal an empire of black money, untaxed and unaccounted for, sapping economic benefit from GDPs of many countries.

Not only do such entities offer repositories from the proceeds of criminal activities, helping crooks wash clean money but in sheltering the fruits of economic activity, they are hiding money from the national accounts of nations. This is money that could be infused into the legitimate economy to stimulate growth, create jobs, and help support vital social services.

We expect such behaviour of self-interested mercantile types but not of our public servants, for if they are not acting in the public interests, who do they work for?

ACKNOWLEDGEMENT:

This piece would not have been possible without the tremendous work of the International Consortium of Investigative Journalists, with over 200 members and hailing from some 70 countries who worked tirelessly and cooperated in collegialy to bring this story to light. In addition, we have quoted from The Guardian, The New York Tmes and Rolling Stone – all which have been attributed in this article.